techUK has released the results of a new wave of our Digital Economy Monitor survey. Data for this poll was collected during the second quarter of 2023, seeking to measure and track operational changes, business performance and how techUK members view the UK’s economic outlook over the next 12 months.

After a challenging downturn in the latter half of 2022, this round of the Digital Economy Monitor reveals a tech sector that is cautious, yet optimistic about its potential to grow.

However, uncertainty over the UK’s economic outlook as well as concerns over investment, infrastructure, and the effects of regulation could cut this optimism short.

When asked about their longer-term ambitions, techUK members want to see their businesses scale and grow; expand into new markets; and improve efficiency, competitiveness, and sustainability. To help them achieve that, they say they need greater incentives to invest in R&D, a more competitive tax regime, and regulatory stability.

Commenting on the results, techUK CEO Julian David said:

2022 presented significant challenges for the tech sector, as soaring energy prices and a talent shortage resulted in a major drop in confidence. However, 2023 has the potential to end on a brighter note, as techUK members revealed a cautious optimism about their growth and investment plans, with many saying they are on track to meet their company’s ambitions.

Still, the tech sector is grappling with uncertainties surrounding the UK’s economic outlook, the impact of regulation, and concerns regarding infrastructure. To unlock the tech sector’s full potential, close collaboration and robust government support are imperative. Together, we can fuel the sector’s growth and supercharge the UK economy, by bringing an additional £200 billion every year.

Julian David CEO

techUK

There were five key themes shown across the survey results:

Business outlook among techUK members has rebounded after a difficult 2022, however techUK members see wider economic challenges on the horizon that could threaten their business plans.

Industry still requires greater support for R&D and innovation, while access to infrastructure has become a greater concern.

Sales and investment plans are cautiously looking up, showing that the industry is on the rebound.

Businesses are reorienting to focus on efficiency with reductions in headcount across a range of companies planned.

When asked about their ambitions for the future techUK members are focusing on growth, efficiency, and sustainability but need Government support to get there.

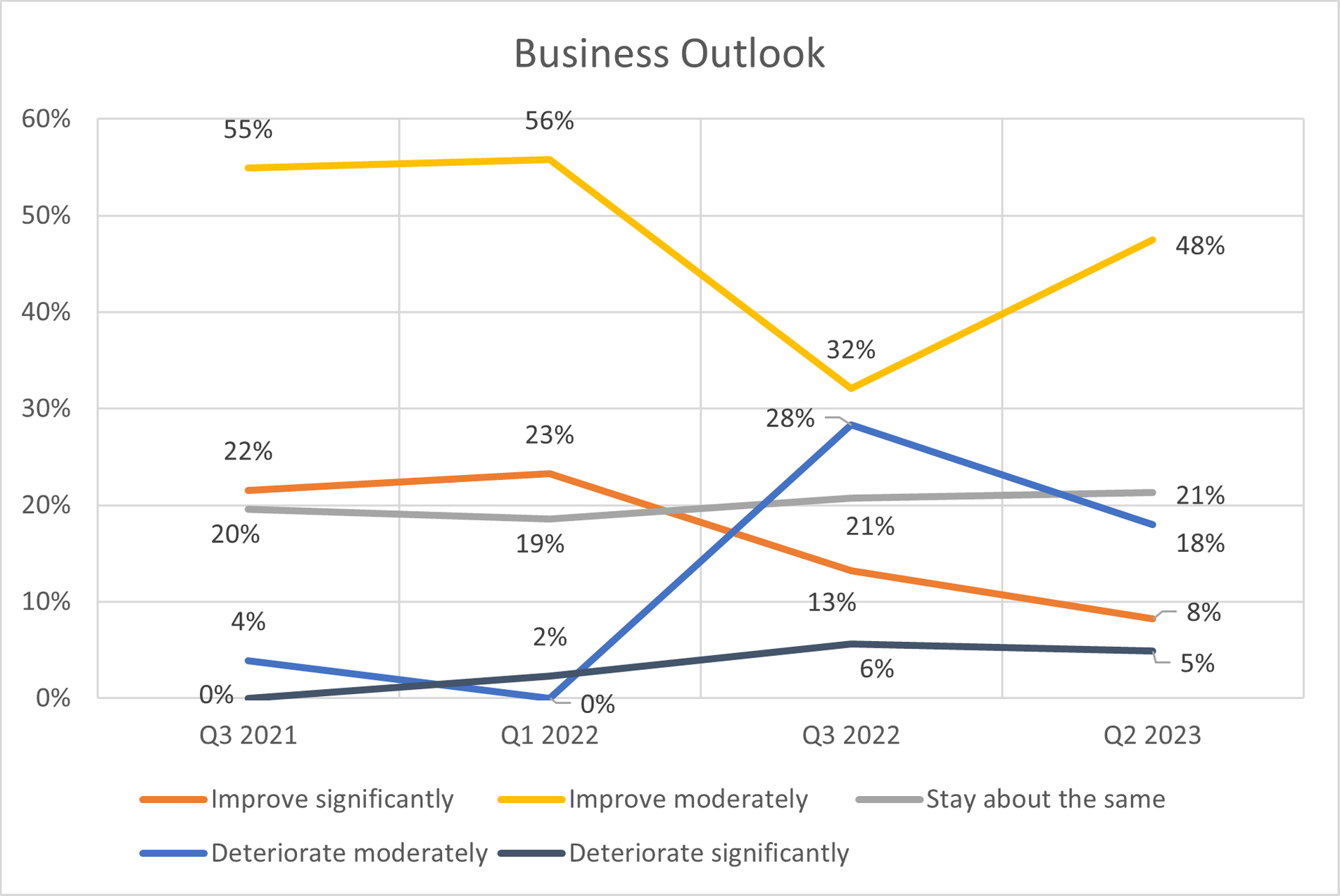

1. Business outlook among techUK members has rebounded after a difficult 2022; however, techUK members see wider economic challenges on the horizon that could threaten their business plans:

When asked about the outlook for business like theirs over the next 12 months, nearly half (48%) of members said they expect it to “improve moderately,” an increase of 16 points from last Monitor. When combined with members who expect conditions to “improve significantly” or “remain the same,” a confident majority of industry (77%) have a stable or positive outlook for industry, an increase from last year (66%).

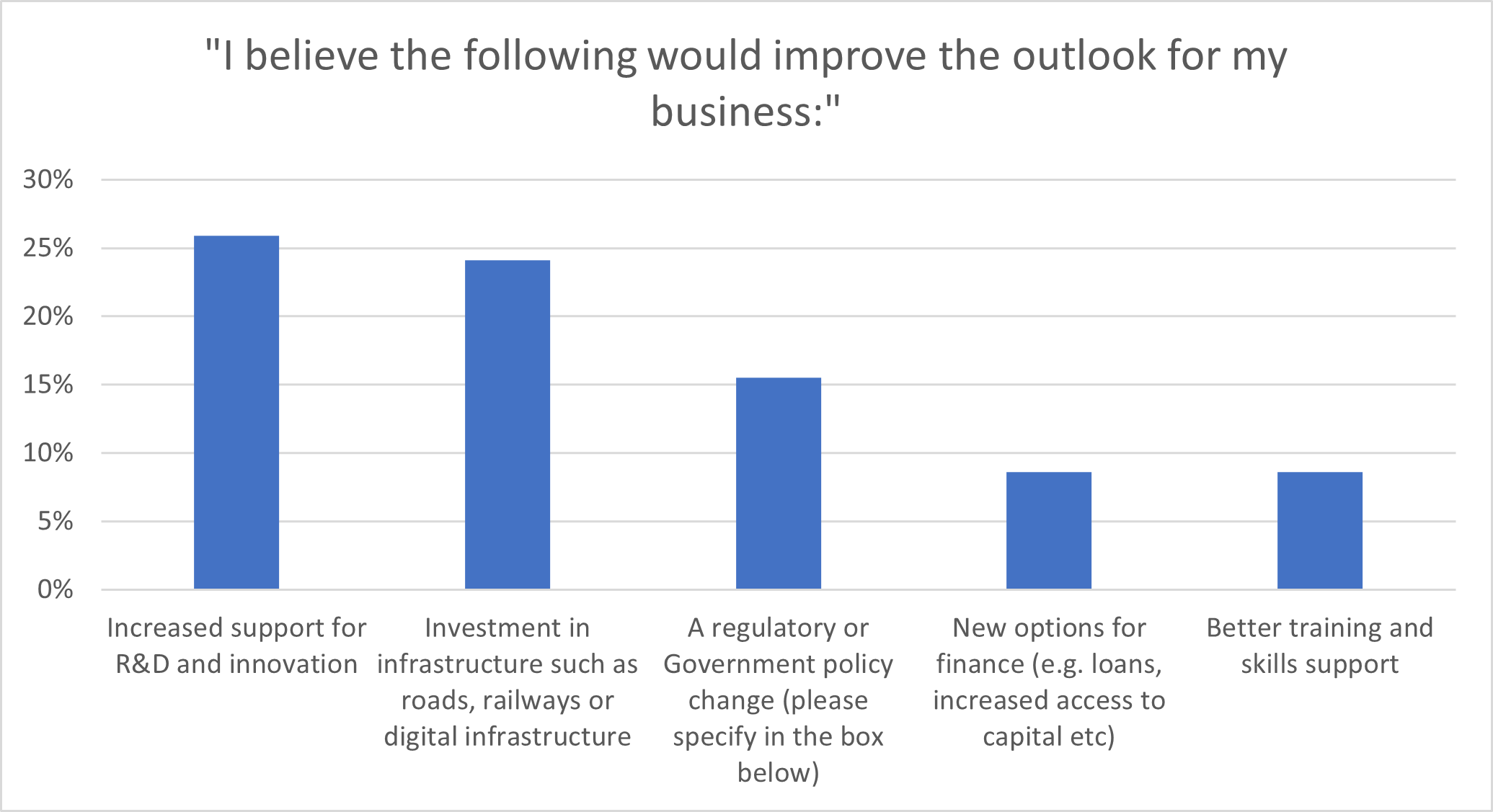

2. Industry still requires greater support for R&D and innovation, while access to infrastructure has become a greater concern:

Government support will be vital for industry to achieve its growth ambitions. When asked what would improve the outlook for their business, members responded that increased support for R&D and innovation (26%), investment in infrastructure (24%), and a regulatory or Government policy change (16%)

R&D support for industry has been subject to cuts and instability since the last Monitor, making it difficult for industry to invest in or plan for innovation. The results echo concerns from industry on the matter, with the need for increased support for R&D and innovation increasing by 10 points to 26%, the top response for the fourth time in a row.

Not far behind is industry’s request for investment in infrastructure, which experienced a drastic increase in responses from just 4% last Monitor to 24% in this one. As captured in techUK’s recently launched UK Tech Plan, many members have challenges around securing sites for manufacturing or operations, increased energy costs for energy-intensive sectors, and how limited digital infrastructure prevents access to talent and/or consumers.

Additionally, 16% of respondents indicated that a regulatory or Government policy change would help to improve the outlook for their business. When asked to elaborate, respondents supported increasing public sector and capital spend, reinstatement of a more favourable R&D tax credit regime, and support for digitalisation and digital adoption, alongside requests to reverse burdensome increases in corporate tax rates and to simplify procurement processes.

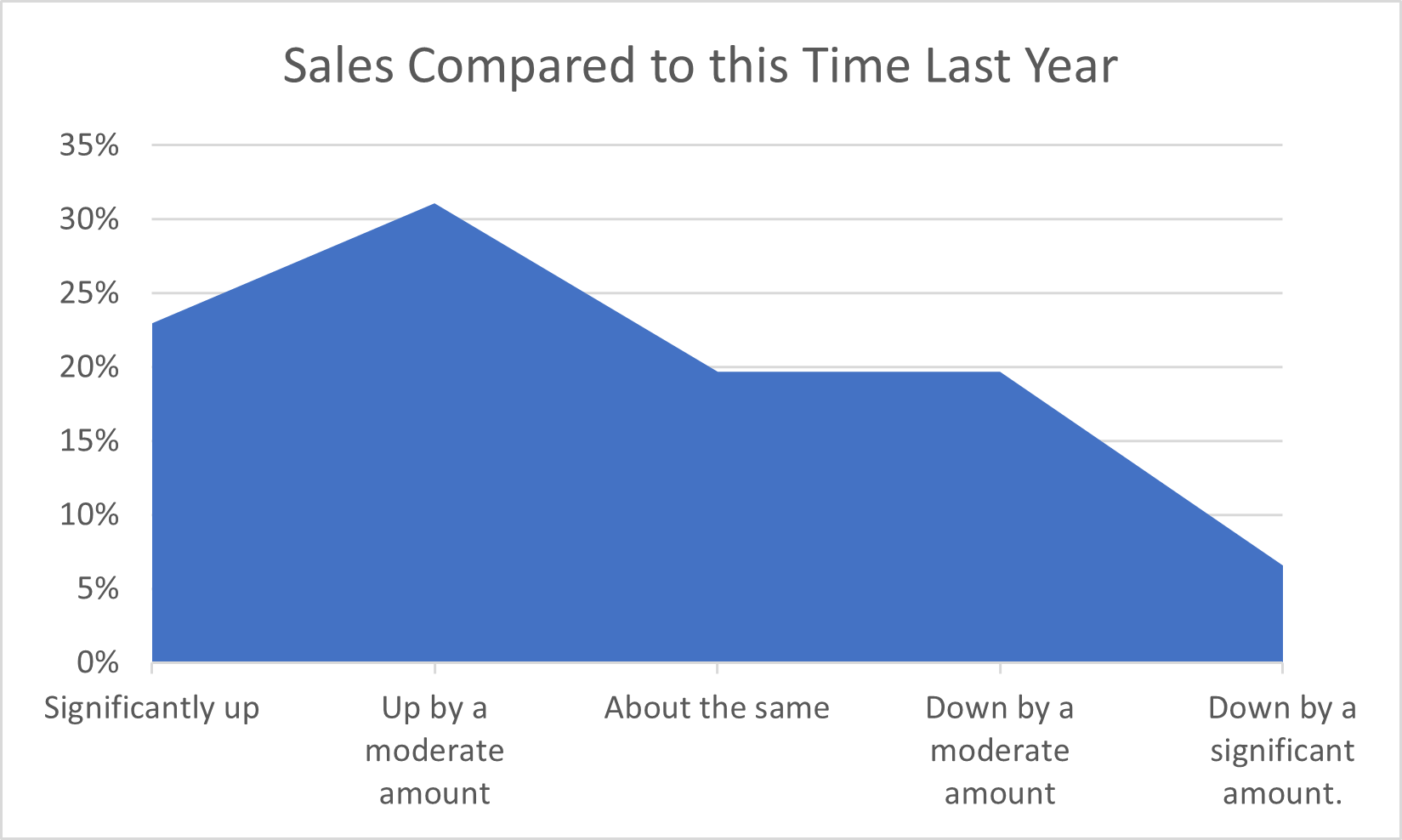

3. Sales and investment plans are cautiously looking up, showing that the industry is on the rebound

Sales and investment plans are weathering the economic storm, albeit with reservations.

The outlook for sales is highly variable space in the sector, with the amount of respondents who said their outlook for sales remained the same as last year dropped by 14 points to just 20%.

This drop was driven by an increase in respondents who said their sales were “up by a moderate amount” (from 26% to 31%) as well as those who said their sales were “down by a moderate amount” (from 13 to 20%). Overall, a majority of respondents (54%) indicated that their sales were up by compared to this time last year.

When asked what the principal reason for sales being up, down, or the same, members responded an increase in investment and interest in our area of operations (33%), changing consumer behaviour (19%), and changes in supply changes (19%).

For investment, member responses indicated that industry is looking to make steady, measured growth in their UK presence, with a majority (57%) of respondents planning to increase investment in business operations in the UK. The proportion of members whose planned investments were significantly up from the year before fell from 21% to 15%. While those whose plans were “up by a moderate amount” rose from 34% to 43%.

The total “up” category (57%) is below the survey’s historical record of 70% in Q1 2022, but is still an increase of 2 percentage points from the last round of the Monitor.

However, there are big differences between respondents with some businesses harder than others. 18% of respondents indicated their plans to invest in their UK operations are “down” when compared with last year, despite an overall improvement.

4. Businesses are reorienting to focus on efficiency with reductions in headcount across a range of companies planned:

Though other metrics like investment plans, sales, and outlook had positive signs or trends, industry’s plans for their headcount reveal the burden of economic challenges, which have created a greater focus on efficiency within companies.

Plans to reduce headcounts have increased from just 2% of respondents in Q3 2021 to 15% in this iteration of the Monitor. This was also double the number who reported plans to reduce heading count in the last Monitor (7%).

Still, a majority of members (57%) do plan to increase headcount in the next year, although there has been a shift from plans to significant increase headcount (down by 6%) to moderate (up by 5%).

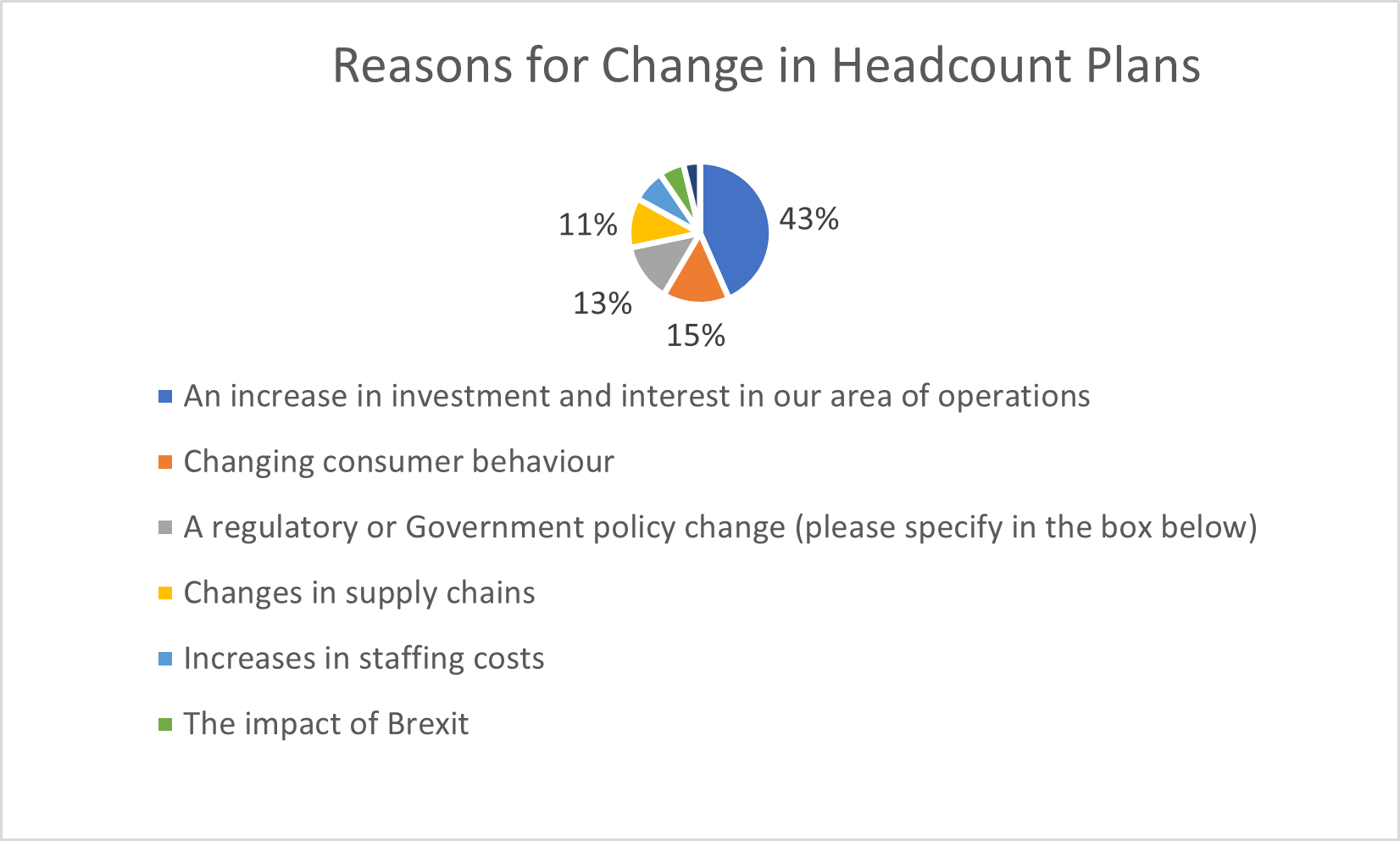

Members planning to increase their headcount cited positive economic changes and natural company growth as a reason, while members planning to decrease their headcount cited economic challenges, the effects of Brexit, and changes in consumer behaviour.

Overall, the main factors cited by members for their headcount plans include changes in investment and interest in their area of operations (43%), changing consumer behaviour (15%), and regulatory or Government policy changes (13%). Notably, the percent of respondents who connected headcount plans to the impact of energy prices dropped from 9% to 0%.

5. When asked about their ambitions for the future, techUK members are focusing on growth, efficiency, and sustainability but need Government support to get there:

In this round of the Digital Economy Monitor, techUK assessed industry’s medium term ambitions, revealing an industry that is ready to be part of the future of the UK economy if we can get the policy and regulatory landscape right.

When asked what longer-term ambitions members had, respondents shared a focus on scaling and growth (30%), expanding within their existing markets or into new markets (24%), and improving efficiency and competitiveness (12%).

When asked if they were on track to achieve these ambitions, almost half of respondents indicated that they were on track to achieve most of them (46%), and an additional 43% of respondents shared that they were on track to achieve some, with only 12% of respondents sharing that they were on track to achieve only a few.

The challenges that respondents indicated were holding back their ability to achieve their ambitions were related to challenges in the larger macroeconomy, with 24% of respondents denoting economic challenges, 19% citing increases in staffing costs, and an additional 19% sharing the impact of Brexit as a challenge.

techUK also asked what members need to make a long-term investment case to grow and expand their business in the UK, and respondents selected greater incentives to invest in R&D (16%), a more competitive tax regime for business (15%), and a more stable regulatory environment (13%).

The Digital Economy Monitor is a survey of techUK members. In this wave of the survey, 64 companies from the industry participated. 36% of respondents were large firms and 64% SMEs. The data was collected from April 24th to May 26th, 2023.

Margherita Certo

Head of Strategic Communications, techUK

Margherita Certo

Head of Strategic Communications, techUK

Margherita is the Head of Strategic Communications at techUK, leading the organisation’s external and internal communications strategy and serving as the primary point of contact for media enquiries.

She is responsible for strengthening techUK’s voice across the technology ecosystem, ensuring the priorities and perspectives of members are clearly represented in the media. She works across the organisation to align messaging with strategic objectives and enhance techUK’s profile and influence.

Before joining techUK, Margherita worked in public relations across the technology, public affairs and charity sectors. She has delivered evidence-based strategic campaigns and built strong relationships with senior stakeholders, helping organisations communicate complex issues with clarity and credibility.

techUK is keeping track of the 2026 updates to the AI Opportunities Action Plan. A full summary of all the announcements this month is forthcoming.Today, the government has announced a £36 million investment to upgrade the DAWN supercomputer at the University of Cambridge, aimed at increasing its computing power sixfold and significantly expanding access to high-performance AI compute in the UK.

The UK has a world-leading regulatory system that supports the economy while protecting the society. However, strategic reforms to the UK’s regulatory regime could help unlock its full potential as a vital catalyst for growth, bringing considerable rewards across industry.