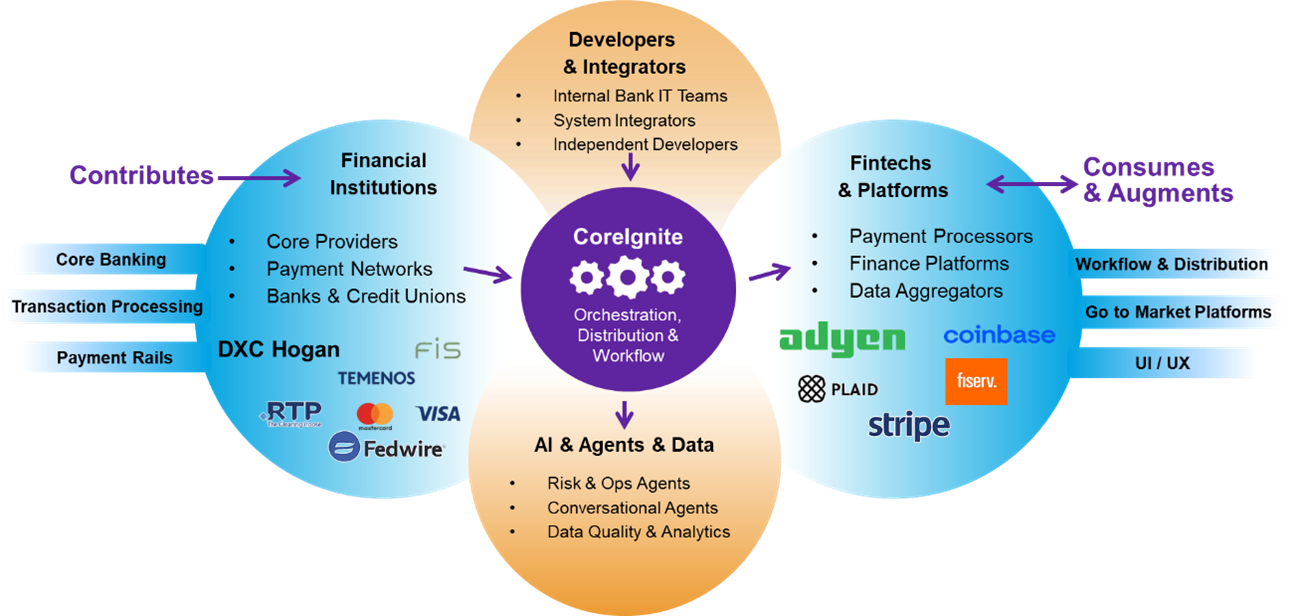

Financial Services Programme activities

The techUK Financial Services programme connects tech firms, the FS industry, and regulators to ensure innovation and technology can be fully embraced. Through market engagement activities and events, we help to empower decision makers and aid collaboration.

Upcoming events

Is Quantum Sensing ready for business adoption?

Digital Catapult, 101 Euston Road, London Partner

Latest news and insights

Learn more and get involved

Financial Services updates

Sign-up to get the latest updates and opportunities from our Financial Services programme.

Meet the team

James Challinor

James Challinor

James leads our financial services programme of activity. He works closely with member firms from across the sector to ensure innovation and technology are fully harnessed and embraced by both industry and regulators.

Prior to joining us James worked at other business organisations including TheCityUK and the Confederation of British Industry (CBI) in roles focused on supporting the financial & related professional services eco-system, with a particular focus on financial technology and market infrastructure.

- Email:

- [email protected]

- LinkedIn:

- https://www.linkedin.com/in/james-challinor-105212177/

Lucas Banach

Lucas Banach

Lucas Banach is Programme Assistant at techUK, he works on a range of programmes including Data Centres; Climate, Environment & Sustainability; Market Access and Smart Infrastructure and Systems.

Before that Lucas who joined in 2008, held various roles in our organisation, which included his role as Office Executive, Groups and Concept Viability Administrator, and most recently he worked as Programme Executive for Public Sector. He has a postgraduate degree in International Relations from the Andrzej Frycz-Modrzewski Cracow University.

- Email:

- [email protected]

- Phone:

- 020 7331 2006

- Twitter:

- @techUK

- Website:

- www.techuk.org

- LinkedIn:

- https://www.linkedin.com/in/lucas-banach-50139650

Sue Daley OBE

Sue Daley OBE

Sue leads techUK's Technology and Innovation work.

This includes work programmes on cloud, data protection, data analytics, AI, digital ethics, Digital Identity and Internet of Things as well as emerging and transformative technologies and innovation policy.

In 2025, Sue was honoured with an Order of the British Empire (OBE) for services to the Technology Industry in the New Year Honours List.

She has been recognised as one of the most influential people in UK tech by Computer Weekly's UKtech50 Longlist and in 2021 was inducted into the Computer Weekly Most Influential Women in UK Tech Hall of Fame.

A key influencer in driving forward the data agenda in the UK, Sue was co-chair of the UK government's National Data Strategy Forum until July 2024. As well as being recognised in the UK's Big Data 100 and the Global Top 100 Data Visionaries for 2020 Sue has also been shortlisted for the Milton Keynes Women Leaders Awards and was a judge for the Loebner Prize in AI. In addition to being a regular industry speaker on issues including AI ethics, data protection and cyber security, Sue was recently a judge for the UK Tech 50 and is a regular judge of the annual UK Cloud Awards.

Prior to joining techUK in January 2015 Sue was responsible for Symantec's Government Relations in the UK and Ireland. She has spoken at events including the UK-China Internet Forum in Beijing, UN IGF and European RSA on issues ranging from data usage and privacy, cloud computing and online child safety. Before joining Symantec, Sue was senior policy advisor at the Confederation of British Industry (CBI). Sue has an BA degree on History and American Studies from Leeds University and a Masters Degree on International Relations and Diplomacy from the University of Birmingham. Sue is a keen sportswoman and in 2016 achieved a lifelong ambition to swim the English Channel.

- Email:

- [email protected]

- Phone:

- 020 7331 2055

- Twitter:

- @ChannelSwimSue,@ChannelSwimSue