The never-ending need for power (Guest blog from Fujitsu)

Guest blog by Fujitsu's Tony Shorthouse, Digital Utility & eMobility Consultant and Shany Mizrahi Otero, Senior Sustainability Consultant, Digital Transformation. Part of techUK's Climate Action at COP28 Campaign Week 2023.

The UK energy landscape is changing

Over the last 5 decades UK household demand for energy has reduced by around 12%, despite a steady population increase of more than 6.5 million. The decline in UK heavy industry has accounted for further demand reduction.[1]

Awareness continues to grow throughout society, industry and governments of the need to change behaviours, to look after the environment and help support the UK government's net zero target by 2050. The introduction of increasingly cost-effective, energy efficient products in both the home and the workplace have also helped reduce our power consumption.

Though we can take positives from this reduction and historical trends, we need to ensure that power generation and grid infrastructure can support future electricity demand which is predicted to increase 50% by 2035, and be 100% higher by 2050. This will primarily be driven by mass adoption of heat pumps and Electric Vehicles (EVs); and the re-introduction of heavy manufacturing, such as Gigafactories to produce EV batteries, and grid power storage. Additionally, given Hydrogen production and the refining process are energy intensive the need for energy to enable this will further increase the demand for power.[2]

Future energy scenarios

Ahead of 2030, power distributors are projecting the need for significantly more infrastructure and more power as organisations accelerate their journey to Net Zero.

Fleet managers are driving the take-up and transition to EVs, including those who operate large fleets of light commercial vehicles, such as final mile couriers, retailers, telecom operators and energy companies.

The result is that our national and localised power transmission networks face ever-increasing demands placed on them from an increasingly technology-led world.

The need to act

Significant demand challenges are derived from the exponential growth of EVs and heat pumps, along with a growing number of renewable energy assets. Likewise, the use of digital technologies, such as AI and cloud computing, are driving more concerns about the energy and environmental impacts of such innovation. Gartner predicts that by 2027, IT leaders will begin facing electricity shortages as IT’s relentless increase in demand for power will outpace the production and supply of energy sources, both renewable and non-renewable.[3]

Industry stakeholders now understand that to upgrade existing infrastructure is hugely expensive, as well as being resource and time intensive. We are witnessing transformational change on a truly industrial scale[4], which in itself will require a significant supply of raw materials and associated power – not least that which is required for the manufacture of steel cables to transmit power.

These aspects represent significant macro-economic factors that only serve to add pressure to the challenging landscape of power generation, distribution and storage: which could take many years to address - requiring billions of pounds of investment - alongside the need to change governmental and regulatory policies and processes. The industry challenges of today for example include at least a three-year delay to connect EV charging sites to the power grid, meaning that it is clear the UK needs a systemic change of approach to ensure its infrastructure is fit for purpose.

This means that for us to move towards Net Zero, and for us to meet our near and mid-term demand, we must find a way to work with the market constraints that exist. We need to find new ways therefore of managing supply and demand, to increase the resilience in our network and to ensure investments that we make now will be able to scale to reap even greater returns in the future.

We believe there is a way, and that is the optimisation and the creation of what we are calling the Digital Energy Spine.

Optimisation in action

In Japan, grid operators have worked with Fujitsu on innovative ways to extend the life of the existing power grids, and optimise the supply of power to better match demand by, such as utilising weather patterns to adapt the load capacity limits of power lines. Whilst this works in Japan, we recognise the diverse nature of global power infrastructure means the investment needed for the UK market would challenge near-term returns; however the solution does illustrate how embracing technology has a real part to play in making a difference. Moreover, these solutions can be combined with climate change resilience analysis; for instance to help us understand the hotspots affected by extreme weather, allowing for appropriate adaptation and mitigation measures, across industries and their supply chains.

Without optimising what we already have - or what is just around the corner - we risk as a country being left behind and being reliant on other nations. For the UK, there remains nothing more than a growing sense of urgency to establish a national programme of infrastructure asset reinforcement, and digitalisation of operational assets. Such long-term, complex programmes of infrastructure replacement are both extensive in nature and cost; hence the need for a coordinated approach enabled through the Digital Energy Spine.

Our short term vision

Through the creation of the Digital Energy Spine, comprising of the initial elements of an integrated energy ecosystem, there is the opportunity to provide alternative scalable proposals to optimise supply and demand, getting more from what we already have.

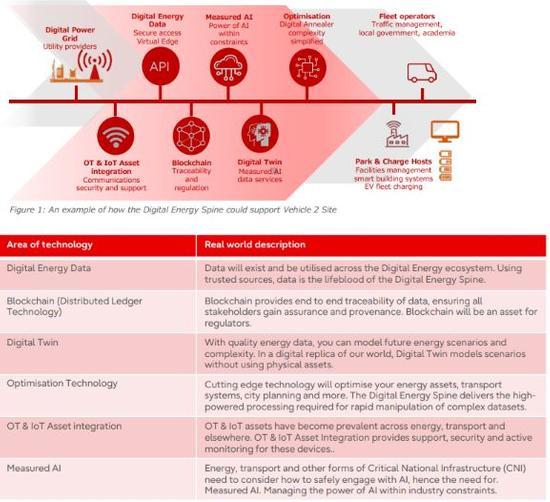

Digital Energy Spine

The Digital Energy Spine is made-up of six core technology elements that can each be embraced stand-alone, or collectively. These are: Digital Energy Data, Blockchain, Digital Twin, High Performance Optimisation, Security and Measured AI.

The real world meets the digital world

These technologies can come together with existing grid assets – and new assets such as EV charging and mid-level generation capabilities – to create near endless opportunities to create new business models and to help balance and optimise the supply and demand of what we already have.

By building and optimising what we have today, not only can we make best use of existing investments - infrastructure and resources - we can also learn to ensure we are ahead of the transformation that is coming when the wider macro investments are in-place; resulting in critical market making advantages both now and in the future.

Furthermore, by combining these capabilities, it is not only possible to track energy demand and supply, but also to accommodate the climate change resilience mechanisms within your 5, 10, 20 year plans, accounting for different weather scenarios and forecasting.

From concept to action

The significant market changes required to achieve Net Zero are mandated upon all of us through the adverse effects we are seeing on our environment and global warming.

The need for change and pace will only increase given more countries will be sure to commit to end the sale of new Internal Combustion Engine vehicles by 2035 or sooner as part of their Net Zero drive, and when further regulations, like clean air zones, are in force.

The drive to EVs therefore will directly translates to the need for more and more infrastructure, in turn increasing the demand for the supply of power. We see three phases towards a fully integrated, end to end Digital Energy Spine.

As an initial phase, widespread adoption of an optimisation flexibility service - such as Vehicle 2 Site (V2S) or Vehicle 2 Building (V2B) - is needed, whilst we await the change in regulations, process and the mass investment needed for the future. Without the optimisation of what we have, the adoption process will continue to be negatively impacted due to the reality of day-to-day operational demands.

The overlapping second phase will see a constant focus on not just the advancement of new technologies and infrastructure deployment, but also on the proving of new business models to both drive revenue and enable operational efficiency gains. This will not be just about new operational models for energy-based companies – they are just the enablers – but will be a holistic approach, encompassing retailers, transport, fleet & logistics, public sector and many other stakeholders. We have seen similar disruptive growth patterns in other industries, such as ride hailing and a multitude of online streaming services. Throughout this time, the right balance needs to be achieved so that the new operational models consider People, Planet and Profit to allow for the UK's decarbonisation journey.

For the final phase, the end-to-end, market integrated Digital Energy Spine will build – with secure data at its heart – on all that has gone before to become a new holistic, dynamic and fundamental part of business growth and our day-to-day lives.

What next?

This whitepaper serves to highlight the size of the challenge – and opportunity – facing the energy industry, and many related industries. There are a series of papers aimed at moving from theory to action, stepping through each through optimisation to creation of the new business models and efficiencies. What this transition means for you, and how Digital Energy Spine can help you with planning and operational changes.

|

References |

Continuing the story, please contact us if your interest is: |

|

[1] BEIS “Energy Consumption in the UK (ECUK) 1970 to 2019”, 2020 [2] BEIS “Decarbonisation of the power sector”, 2023 [3] Gartner “Top Strategic Technology Trends for 2024: Sustainable Technology”, 2023 |

Fleet Management and Commercial Property Management. |

|

Financial or Operational leaders in Retail, Healthcare, Education, Local Authorities, Transport, Office, Fleet & Logistics. |

|

|

For technology innovators looking for more on the Digital Energy Spines technology areas of Digital Energy Data, Blockchain, Digital Twin, Optimisation Technology, OT & IoT Asset Integration and Measured AI. |

techUK - Committed to Climate Action

Visit our Climate Action Hub to learn more or to register for regular updates.

By 2030, digital technology can cut global emissions by 15%. Cloud computing, 5G, AI and IoT have the potential to support dramatic reductions in carbon emissions in sectors such as transport, agriculture, and manufacturing. techUK is working to foster the right policy framework and leadership so we can all play our part. For more information on how techUK can support you, please visit our Climate Action Hub and click ‘contact us’.

Authors

Tony Shorthouse

Shany Mizrahi Otero

Shany Mizrahi Otero - Senior Sustainability Consultant - Fujitsu | LinkedIn