R&D Tax Credits: What has changed? (Guest blog from Liam Hanna, Leyton)

What has changed?

During the Autumn Statement, Jeremy Hunt stated, “I have decided today to cut the deduction rate for the SME scheme to 86% and credit rate to 10%, but increase the rate of the separate R&D Expenditure Credit from 13% to 20%. Despite raising revenue, the OBR has confirmed that these measures have no detrimental impact on the level of R&D investment in the economy. Ahead of the next budget, we will work with industry to understand what further support R&D intensive SMEs may require.” These changes will apply to expenditure incurred on or after 1 April 2023.

Whilst the rate of relief for SMEs will be reduced, in practical terms, the reduction will be largely offset for profitable SMEs by the rise in the headline corporation tax rate to 25%. The shift will be felt mostly by loss-making SMEs, and it is unclear how reducing the funding available to businesses in the start-up/growth/scaling-up phase will help tackle fraud and abuse. Large companies are the clear winners following the most substantive change to the R&D tax relief scheme in 20 years.

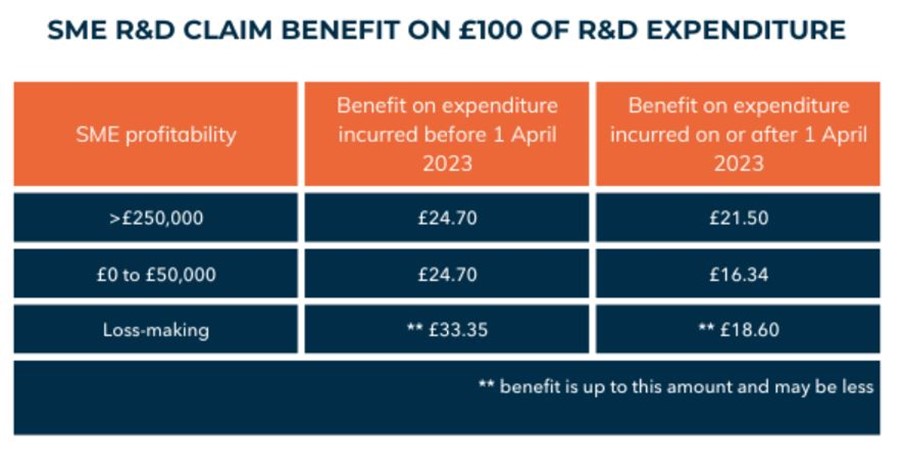

What is the financial impact for SMEs?

The impact for SMEs will depend on their profitability as set out in the below table.

The corporation tax rate is set to increase from 1 April 2023. This impacts the benefit of the R&D claim. The rate will increase to 25% for companies whose taxable profits exceed £250,000. For companies with profits of less than £50,000, the current 19% rate will still apply. Companies with taxable profits between £50,000 and £250,000 will pay tax on a sliding scale between 19% and 25%.

There are situations in which SMEs may claim under the Research and Development Expenditure Credit (RDEC) scheme. This can occur where a business has received certain types of grant funding or if the SME has carried out the R&D as a subcontractor. Indeed, we may see more SMEs making claims under RDEC due to HMRC’s recent shift in interpretation to their guidance regarding the identification of subcontracted expenditure. This issue was highlighted in the CIOT Public Policy Director’s recent statement that “HMRC have in recent times been changing their interpretation of the existing rules of the more generous SME scheme in ways that are capable of acting almost as ‘catch-all’ provisions to deny relief”. As explained below, the RDEC regime is now set to become significantly more generous, with the Autumn Statement changes effectively levelling the SME and RDEC schemes.

What is the impact for large businesses and claims made under RDEC?

Jeremy Hunt gave some reassurance when he said, “I want to go further, so today I protect our entire research budget and confirm that we will increase public funding for R&D to £20 billion by 2024-5 as part of our mission to make the United Kingdom a science superpower.” This represents a substantial increase. It would be safe to assume that the majority of innovation funding will therefore be redistributed to large businesses making RDEC claims.

The RDEC rate will increase from 13% to 20%, which equates to a 42% increase in benefits. The net benefit on £100 of R&D expenditure is set out below.

- Benefit on expenditure incurred before 1 April 2023 = £10.53

- Benefit on expenditure incurred on or after 1 April 2023 = £15.00

The bigger picture

While the changes are not unexpected, the impact on loss-making SMEs is particularly disappointing. These types of companies tend to be the ones generating the most innovation. Understandably, there has been some backlash from the industry. R&D tax credits are seen as vital for innovative loss-making businesses in the start-up phase. In the current climate, these changes may put the future of these types of businesses at risk. The impact is softened for profitable SMEs paying the higher rate of CT.

These changes represent a move towards aligning the R&D schemes for small and large businesses. While that has unfortunately come at a cost to SMEs, large businesses will benefit from an increased R&D incentive (at least, where that work is being carried out in the UK). This is perhaps driven by a perception that large businesses will provide better value in return for taxpayer investment. It remains to be seen whether that is, in fact, the case; however, it may very likely have been one of the government’s deciding factors in effecting this change.

For anyone interested in finding out more on R&D Tax Credits, please contact Liam Hanna, Team Leader at Leyton. You can also find more analysis and reaction to the Autumn Statement here.

techUK – Supercharging UK Tech and Innovation

The opportunities of innovation are endless. Automation, IoT, AI, Edge, Quantum, Drones and High Performance Computing all have the power to transform the UK. techUK members lead the development of these technologies. Together we are working with Government and other stakeholders to address tech innovation priorities and build an innovation ecosystem that will benefit people, society, economy and the planet - and supercharge the UK as a global leader in tech and innovation.

For more information, or to get in touch, please visit our Innovation Hub and click ‘contact us’.