Open Banking, why was Martin Lewis wrong?

Back in June 2018 Martin Lewis (UK Money Saving Expert) sat on the This Morning breakfast show sofa and explained how the new Open Banking regulations would herald a revolution in retail banking. In short, he explained how banks will now need to share data, meaning customers would be able to not only move their money far more easily to those providers delivering the best value, but also banks will be able to provide far greater financial support. The example he gave was on how banks would be able to advise on your utility bills and cost of living. If only that were the case given today’s financial challenges!

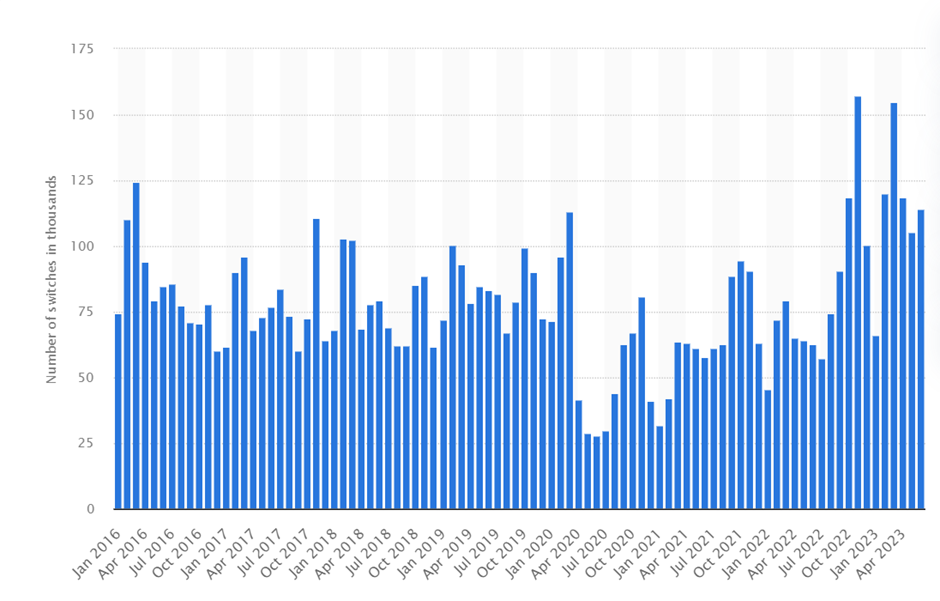

The following graphic by Statista shows no discernable change in customer mobility since January 2016. So since the introduction of Open Banking the retail banking revolution suggested and account mobility has clearly not happened. Why is that?

Number of customers switching their current bank account providers in the United Kingdom (UK) from January 2016 to June 2023;

Source: https://www.statista.com/statistics/417397/number-of-switching-current-bank-accounts-uk/

The reason lies in how banks are structured. Talk to any of the traditional high street banks and they are broadly structured in the same way, with line of business divisions responsible for mortgages, current accounts, loans, insurance etc. supported by central functions such as risk and credit. Each of these divisions also have their own infrastructure and data which, over time, have grown significantly due to the volume of data accumulated. If you consider an average mortgage lifespan of 25 years, then you can imagine the amount of data held over, say, a 35 year period.

These organisational silos, with their huge data repositories, find it almost impossible to collaborate especially when you factor in the need for real-time decision making. The outcome being that the banks cannot quickly establish our relationship with the bank in terms of products held, length of relationship, debit/credit positions etc. This also has the impact of making it very difficult to provide any meaningful insight into spend by category i.e. utilities, mortgage, savings, entertainment etc. across multiple accounts and/or products. This therefore makes access to our financial data from other financial institutions a moot point. If banks cannot get a unified view of our financial position from their own sources then adding yet more sources delivers no real value. Therefore banks find it almost impossible to provide the level of financial insight and services that Martin Lewis described in his interview. This is also the same reason we are not presented with personalised products, i.e. a mortgage with built-in insurance and interest offset by savings.

However, as is often the case, there is an answer to the technical challenges. These large data silos can be unified by approaching the problem logically rather than physically. In other words, rather than trying to consolidate large volumes of data into yet another large repository, abstract above those physical systems and work within a logical framework. This is achieved by adopting data virtualisation. The Denodo Data Virtualisation platform enables enterprises to access any data source and query the data in real time without replicating or moving the data. This of course does not address any organisational silo issues.

What this means is, not only are there operational gains to be achieved by a bank such as migrating of legacy systems, moving to cloud or consolidating data sources but more meaningfully banks will be able to create data models that would support real-time analysis of spend, particularly when a customer opts into Open Banking. This in turn would mean that banks would be able to offer the kind of insight into our financial affairs that would help with managing the cost of living and offer personalised products at a time when most needed.

To summarise, we should be demanding that our banks address those technical challenges, begin to offer a more personalised relationship with truly beneficial insight to our financial activity, and provide the guidance that Martin was suggesting back in 2018.

Reference: Martin Lewis, This Morning interview - https://www.youtube.com/watch?v=3hJtsvSaQ-4

Authors