Business management 4.0 - intelligent automation opens up new possibilities

“What has been available to us through each of the three preceding stages of our industrial revolution has been limited by what business could offer during each period with the tools at its disposal. But now the Fourth Industrial Revolution has delivered business and society a new set of tools to work with, and to reckon with.” - Forbes

The vision for industrial processes alluded to in this quote is increasingly a reality in the insurance industry. Signs of this are everywhere, including the chatbots that are already widely used in customer communication and the automated processes that support claims handlers. And while these are relatively recent developments, a large part of the process from the application, through the creation of the contract in the policy management system, to the creation and sending of the insurance policy to the customer, has been automated for a number of years.

However, an essential part of the insurance value chain - business management - is still waiting to be awakened from its slumber.

Targeting strategy and profitability

A root cause of this is that, in many companies, business management is not a distinct function. Every insurer has units such as ‘operations’, ‘product management’ and ‘claims processing’, but there is rarely a ‘business management’ function. Even where there is, most tend to focus more on the past than on the use of actuarial forecasts to predict future developments.

But the aim of ‘business management’ in the insurance context is specifically to balance the strategic goals of the company in terms of profitability on the one hand and inventory volume on the other, taking account of both new business and existing business equally. It is, by definition, forward looking. So how can intelligent automation support these goals?

To illustrate the possibilities, we’ve drawn up a property and casualty (P&C) insurance example. However, the options could easily be transferred to life and health insurance.

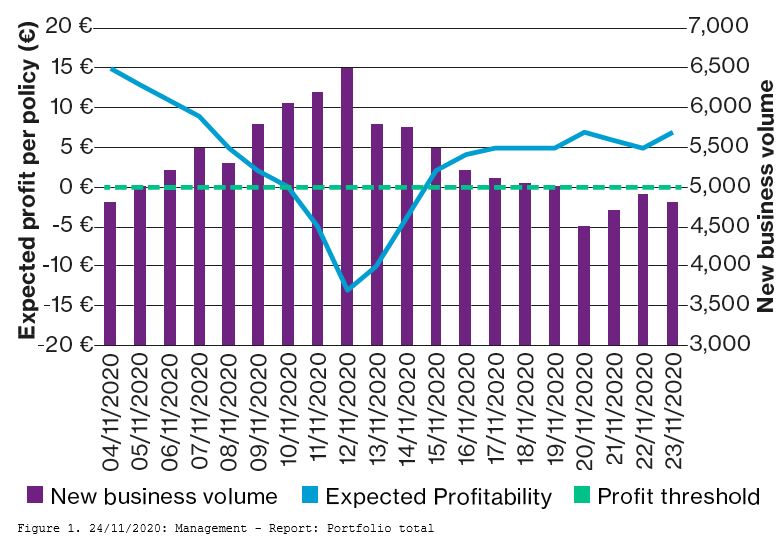

Figure 1 above shows a report of new business volumes and expected profitability per policy for a fictitious insurance company over a 20-day period in November 2020. With well-targeted and appropriate automation, the management team will receive the report on the morning of 24 November.

This kind of automated reporting is made increasingly possible with suitable software (such as Willis Towers Watson Unify and Radar), without great effort and without the need to call on already overloaded IT personnel.

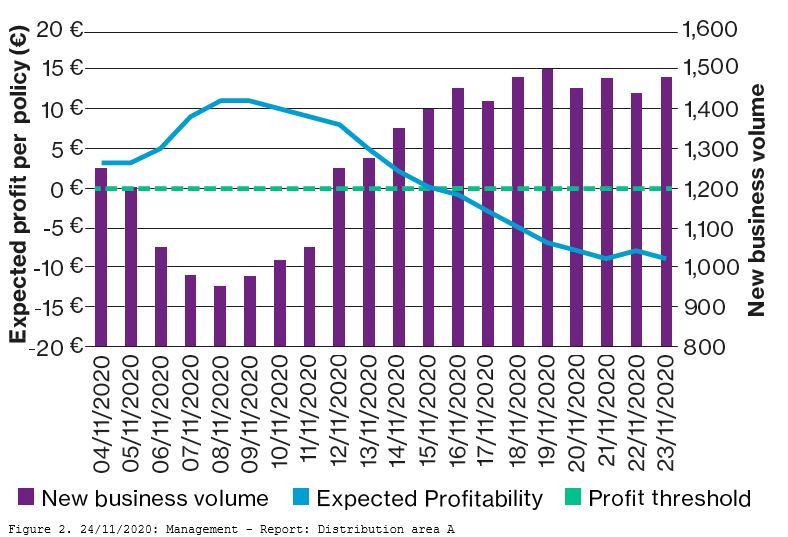

The value of such a report is threefold. First, it provides valuable management information and can be sent at a chosen period and frequency - daily if required - to those who, regardless of department, are responsible for business management in the company. Second, with appropriate automation, the report can be created fully automatically, without tying up any employee capacity. Without automation, responsibility for creating such a report would normally sit with the actuarial department because the expected profitability is an actuarial forecast, drawn up in individual contracts and only presented in aggregated form. And finally, decision makers can ‘immerse themselves’ in the portfolio as much as they want, examining critical points and reacting to them immediately (see Figure 2 below for a hypothetical secondary analysis of a special sales region).

Indispensable high-frequency business management

Beyond the business management information itself, what matters as much, if not more, is how companies are able to respond to it. Here is where automation in insurance can really come into its own.

In the example, the question arises: what would happen if the company failed to spot the negative impact on profitability in Figure 1 from 4 November to 12 November because of a lack of appropriate processes or a lack of the right kind of automation? Or what would happen if the prices could not be adjusted because of a lack of agility? The obvious answer is that, overall, new business from Q4 2020 would probably be highly unprofitable!

However, as this new business would usually be on risk from January 2021, the effects of this problem would only show up in the income statement for 2021, which would normally be generated in spring 2022. In other words, this issue would only come to light around 18 months after the event and without any countermeasures whatsoever having been deployed. And therein lies the case for high-frequency business management.

As convincing an argument as this example may present in its own right, the lack of such analysis is not the only problem that insurers face. Many insurers, for example, when confronted with an adverse development (such as the one shown between November 10 - November 12 in Figure 1), would not be able to react with a corresponding price change sufficiently quickly anyway.

It is worth noting that, through the use of suitable software, increasing numbers of insurers are now actually able to change prices in a very agile manner, without involving their IT departments. Skilful handling of new business data and the existence of high- quality risk models for forecasting profitability are further important prerequisites for this.

What this exemplifies is the importance of first investing in the digitization of sales (including agile price change options) before moving on to think about business management 4.0 more widely.

So, why do we think this concept of business management 4.0 is so important? Quite simply it comes down to competitive advantage or parity. Relevant daily reports improve the management team's decision-making basis for pricing policy. And ultimately, advanced business management with appropriate automation will provide insurance companies with numerous competitive advantages, helping them to correctly assess profitability and pricing, all with the required flexibility and agility.

Fredrik Motzfeldt

GB TMT Industry Practice Leader

You can read all insights from techUK's Intelligent Automation Week here